In its half-yearly Financial Stability Report, the central bank noted that “the overall risk environment remains challenging” amid a sluggish domestic economy, further risks to global growth and inflation and heightened geopolitical tensions.

The Bank of England hiked interest rates by more than 500 basis points between December 2021 and August 2023, taking its main rate to a 15-year high in a bid to combat soaring inflation. Its Financial Policy Committee highlighted in the report that long-term interest rates in both the U.K. and the U.S. are now around their pre-2008 levels.“The full effect of higher interest rates has yet to come through, posing ongoing challenges to households, businesses and governments, which could be amplified by vulnerabilities in the system of market-based finance,” the FPC said.“So far, and while the FPC continues to monitor developments, U.K. borrowers and the financial system have been broadly resilient to the impact of higher and more volatile interest rates.”

Yet economists have noted that external demand is still relatively weak, and that policy support from Beijing that focuses on the supply side will struggle to make inroads into reigniting domestic demand to compensate.

Neumann told CNBC’s “Squawk Box Europe” on Thursday that the Chinese economy remains weak, and that the positive export figure, released earlier Thursday, should be taken with a pinch of salt.

“Some of the Asian numbers have looked better on the trade front — Korea as well, Taiwan, for example — but this is a lot of inventory adjustment coming through the global system,” he noted.

“There’s not going to be follow-through on the export side in the next few months, and of course on the domestic side with imports contracting again, that just highlights that there is still a steep hill to climb when it comes to generating that accelerating growth in mainland China.”

This global inventory adjustment, particularly among U.S. importers, combined with base effects pushing up the numbers, means the positive export surprise does not necessarily mean exports are accelerating meaningfully, he suggested.

Not that there’s anything wrong with that. A growing economy is a good thing, and nothing underpins that better than a solid labor market. Economists surveyed by Dow Jones expect the Labor Department to report that nonfarm payrolls expanded by 190,000 last month, up from the 150,000 in October.

But investors and policymakers have been expecting things to slow down enough to at least allow the Federal Reserve to call an end to this cycle of interest rate hikes as inflation ebbs and the supply-demand mismatch in employment evens out.

A hot jobs report could undermine that confidence, and put a damper on what has been a buoyant mood on Wall Street.

“There’s some risk to the upside because of the returning auto workers who were on strike,” said Kathy Jones, chief fixed income strategist at the Schwab Center for Financial Research. “So it looks like a steady but slowing jobs market.”

Payroll growth has averaged 204,000 over the past three months, a solid gain though well below the 342,000 level for the same period in 2022. The unemployment rate over the past 12 months, however, has risen just 0.2 percentage point to 3.9%, elevated from where it was earlier in the year but still characteristic of a robust economy.

However, there are a number of dynamics at play in the current picture that make this week’s report, which is scheduled to be released at 8:30 a.m. ET, potentially critical.

Average hourly earnings are expected to show acceleration of 0.3% from October and 4% over the 12-month period, according to Dow Jones.

The yearly average hourly earnings level is not consistent with the Fed’s 2% inflation goal, but it is off its March 2022 peak of 5.9%. Getting wage growth to a sustainable level is vital to bringing inflation down, so anything more pronounced could generate a market reaction.

“When you come down to trying to measure supply and demand, price is probably the most accurate way to look at it, and you know that wage growth has slowed considerably,” Jones said. “So it tells you supply and demand are coming back on track.”

Though the jobless figure has risen just incrementally from a year ago, it’s up half a percentage point from its recent low of 3.4% in April.

The difference is significant in that a time-tested indicator known as the Sahm Rule shows that when the unemployment rate rises half a point from its most recent low on a three-month average, the economy is in recession.

British think tanks the Institute For Public Policy Research and Common Wealth said in a report Thursday that big firms made inflation “peak higher and remain more persistent,” particularly within the oil and gas, food production and commodities sectors.

“We argue that market power by some corporations and in some sectors – including temporary market power emerging in the aftermath of the pandemic – amplified inflation,” the report said.

The author’s analysis of financial reports from 1,350 companies listed in the U.K., U.S., Germany, Brazil and South Africa found nominal profits were on average 30% higher at the end of 2022 than at the end of 2019.

This does not necessarily mean that overall profit margins have risen, but it does mean that higher prices have been shouldered by consumers, the authors said.

“Companies with (temporary) market power seemed to be able to protect their margins or even reap ‘excess profits’, setting prices higher than would be socially and economically beneficial,” they wrote.

The report stresses that corporate profits were not the sole driver of inflation and did not cause the energy market shock following Russia’s invasion of Ukraine in February 2022. But the report authors argue that so-called “market power” has not been sufficiently captured in the current debate around the causes of inflation, particularly when compared with the impact from the labor market and rising wages.

“In an energy shock scenario, if costs were equally shared between wage earners and company owners, one would expect the rate of return to fall as firms do not increase prices fully to make up for higher costs, and wage earners do not fully keep up with inflation. But this is not what happened. A stable rate of return – for example, as seen in the UK – suggests pricing power by firms, which allowed them to increase prices to protect their margins,” it said.

Glencore declined to comment when contacted by CNBC. The other companies did not respond.

Inflation began a steady march higher in mid-2020 amid a host of factors including global supply chain constraints, volatile food production conditions, tight labor markets, pandemic stimulus measures and the Russia-Ukraine war.

The impact of so-called “greedflation,” or companies raising prices more than needed to protect margins from higher input costs and market movements, has been contested.

But what constitutes “greedflation” is not an exact science. This year, the boss of U.K. supermarket giant Tescosuggested that some food producers may be raising prices more than necessary and fueling inflation, a claim that was strongly denied by the industry.

A blog posted by economists at the Bank of England in November found “no evidence” of a rise in overall profits among companies in the U.K., where they say prices have risen alongside wages, salaries and other input costs, with a similar picture in the euro zone.

“However, companies in the oil, gas and mining sectors have bucked the trend, and there is lots of variation within sectors too – some companies have been much more profitable than others,” they wrote.

China’s Politburo said it would continue to implement “proactive” fiscal policies and “prudent” monetary policies next year, in a bid to bolster domestic demand.

Chaired by Chinese President Xi Jinping, the Politburo’s Friday meeting analyzed the economic work to be undertaken in 2024. It pledged to effectively enhance “economic vitality,” to prevent and defuse risks and to consolidate and enhance the upward trend of an ailing recovery in the world’s second-largest economy.

China’s Politburo said that “proactive fiscal policy must be moderately strengthened, improve quality and efficiency, and the prudent monetary policy must be flexible, appropriate, precise and effective.”

Lost momentum

Demand for Chinese goods has fallen this year as global growth slows, stoking concerns about Beijing’s ability to mount a robust post-pandemic recovery. Momentum has taken a hit from a slew of factors, including the country’s beleaguered property market, sluggish global growth and geopolitical tensions.

HSBC’s chief Asia economist, Frederic Neumann, told CNBC on Thursday that the Chinese economy is unlikely to be bolstered by further fiscal stimulus and still has a “steep hill to climb,” even after a surprise pickup in exports.

Economists have noted external demand in China is still relatively weak and warned that policy support that focuses purely on the supply side will likely not be enough to achieve lasting results.

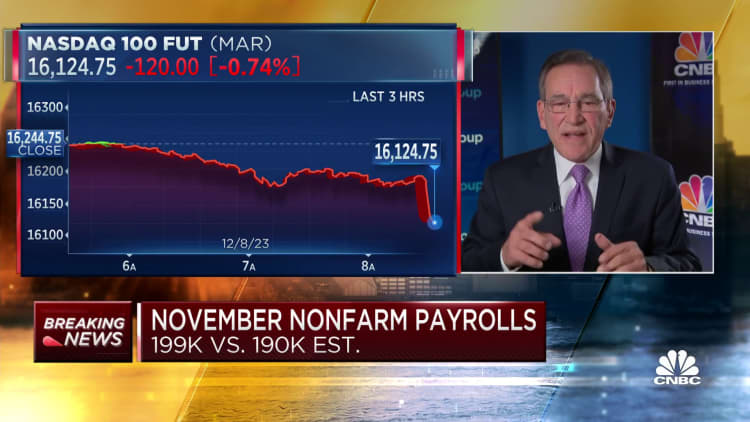

Nonfarm payrolls rose by a seasonally adjusted 199,000 for the month, slightly better than the 190,000 Dow Jones estimate and ahead of the unrevised October gain of 150,000, the Labor Department reported Friday. The numbers were boosted by sizeable gains in government hiring as well as workers returning from strikes in the auto and entertainment industries.

The unemployment rate declined to 3.7%, compared with the forecast for 3.9%, as the labor force participation rate edged higher to 62.8%. A more encompassing unemployment rate that includes discouraged workers and those holding part-time positions for economic reasons fell to 7%, a decline of 0.2 percentage point.

“The job market continues to be resilient after a year of dodging recession fears,” said Daniel Zhao, lead economist at job ratings site Glassdoor. “Really the one concern that we had coming in today’s report was the recent rise in the unemployment rate. So the improvement in unemployment was a welcome relief.”

Average hourly earnings, a key inflation indicator, increased by 0.4% for the month and 4% from a year ago. The monthly increase was slightly ahead of the 0.3% estimate, but the yearly rate was in line.

“What we wanted was a strong but moderating labor market, and that’s what we saw in the November report,” said Robert Frick, corporate economist with Navy Federal Credit Union, noting “healthy job growth, lower unemployment, and decent wage increases. All this points to the labor market reaching a natural equilibrium around 150,000 jobs [per month] next year, which is plenty to continue the expansion, and not enough to trigger a Fed rate hike.”

https://datawrapper.dwcdn.net/Xb12F/1/

Health care was the biggest growth industry, adding 77,000 jobs. Other big gainers included government (49,000), manufacturing (28,000), and leisure and hospitality (40,000).

Heading into the holiday season, retail lost 38,000 jobs, half of which came from department stores. Transportation and warehousing also showed a decline of 5,000.

Duration of unemployment fell sharply, dropping to an average 19.4 weeks, the lowest level since February.

Though growth defied widespread expectations for a recession this year, most economists expect a sharp slowdown in the fourth quarter and tepid gains in 2024. Gross domestic product is on pace to rise at just a 1.2% annualized pace in the fourth quarter, according to an Atlanta Fed data gauge, and most economists expect growth of around 1% in 2024.

The job gains for health care and social assistance rise to 99,000 when including private education, as some economists do.

Much of the labor market story over the past two years has been tied to the economic rebound from the Covid-19 pandemic, but the health-care growth appears to be part of a longer-term trend.

“We’re back to 2019 in some ways. If prior to the pandemic, you would have said, ‘Hey, health care’s going to be one of the largest sources of hiring in late 2023,’ no one would have been surprised by that, I think. There are very long-term structural tailwinds here,” Nick Bunker, director of economic research at Indeed Hiring Lab, told CNBC.

Bunker also pointed out that health care is less sensitive to higher interest rates or other cyclical factors that affect the U.S. labor market.

Manufacturing employment rose by 28,000, helped by the 30,000 jobs gained in motor vehicles and parts as the United Auto Workers strike ended. The information sector was also bolstered by the addition of 17,000 jobs from the motion picture and sound recording industries, as Hollywood production restarts after the actors’ strike was resolved.

Retail trade was an outlier area to the downside, losing more than 38,000 jobs. The sector is roughly flat year over year in terms of total jobs, according to the Labor Department.

“I’m not spooked by it right now. … If you look at the nonseasonally adjusted gains for that sector, it’s roughly in line with what we saw last year. So maybe the seasonal adjustments need to catch up or change. I think we’ve seen this with a variety of data,” Bunker said.

For white Americans, the jobless rate fell 0.2 percentage points to 3.3%. Hispanic Americans also saw their unemployment rate slip 0.2 percentage points to 4.6%.

“That uptick in unemployment is not because more Asian workers are flooding into the labor market, feeling optimistic about getting jobs. It’s actually accompanied by a fall in participation as well as a fall in employment,” Elise Gould, senior economist at the Economic Policy Institute, told CNBC.

The unemployment rate for Black Americans — the demographic with the highest jobless percentage in the U.S. — held steady last month at 5.8%. The jobless rate for Black men age 20 or older spiked more than 1 percentage point to 6.4% from October’s 5.3%. That said, those gains came as the participation rate for this cohort increased to 69.2% from 67.5%.

“The rise in unemployment is because more workers are optimistic, coming back in or entering the labor market for the first time, and many of them are finding jobs. And many of them are not, which is why the unemployment rate went up,” Gould added.

Black Americans were hit harder by business shutdowns during the Covid-19 pandemic. The unemployment rate for Black workers peaked at 16.8% in 2020, versus the overall unemployment rate’s April 2020 high of 14.7%.

Gould added the caveat that the Asian workers in the survey made up a relatively smaller demographic group, and that both of these series are incredibly volatile from month to month.

However, such gauges can be “fluky” and are not in line with some other signals coming from consumers, said Liz Ann Sonders, chief investment strategist at Charles Schwab. Debates over soft landings and inflation expectations and interest rate outlooks tend to miss bigger points, Sonders added.

Prior to 2023, Sanders and Schwab had been stressing the notion of “rolling recessions,” meaning that contractions could hit certain sectors individually while not dragging down the economy as a whole. The distinction may still apply heading into 2024.

“The recession versus soft landing debate sort of misses the necessary nuances of this unique cycle,” Sonders said. “A best-case scenario is not so much a soft landing, because that ship has already sailed for [some] segments. It’s that we continue to roll through such that if and when services gets hit more than the brief ding so far and it takes the labor market with it, you’re already in stabilization or recovery mode in areas that already took their big hits.”

After all, there’s nothing about a 3.7% unemployment rate and another 199,000 jobs that even whispers “recession,” let alone screams it.

At least for now, then, the U.S. economy can take another win with a small “W” as it looks to navigate through what had been the highest inflation level in more than 40 years — and a still-uncertain path ahead.

“Overall, the jobs market is doing its part to get us to a soft landing,” said Daniel Zhao, lead economist at jobs rating site Glassdoor. “It’s boring in all the right ways. That’s a welcome change after a few years of less-boring reports.”

The level of job creation was just above the Wall Street estimate of 190,000. Average hourly earnings rose 4% from a year ago, exactly in line with expectations. The unemployment rate unexpectedly declined to 3.7%, easing worries that it could trigger a historically dead-on signal known as the Sahm Rule, which coordinates increases of the unemployment rate by half a percentage point to recessions.

Still, the solid report couldn’t dispense the lingering feeling that the economy isn’t out of the woods yet. The fear primarily comes from worries that the Federal Reserve’s aggressive interest rate increases haven’t exacted their full toll and still could trigger a painful downturn.